Fiscal Policy & the Government Budget

Week 11

May 4, 2026

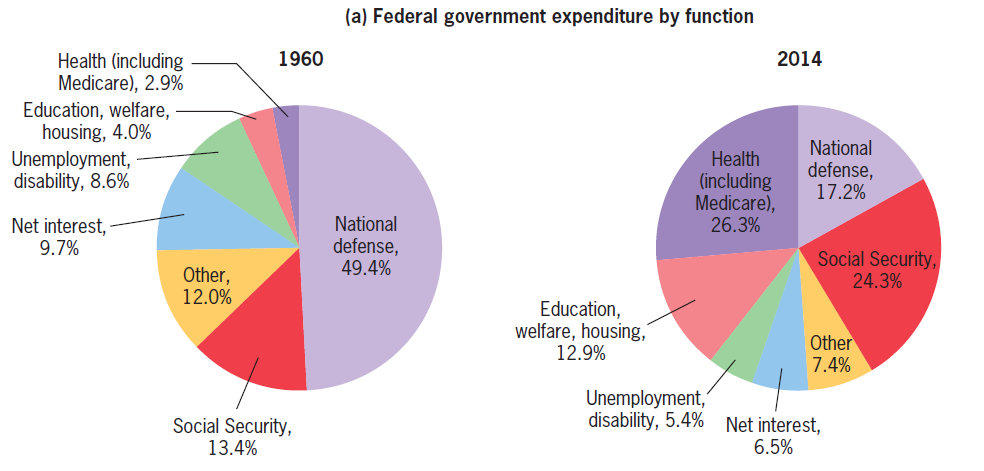

Federal Government Spending: 1960 vs 2014

From: Jonathan Gruber (2016). Public Finance and Public Policy, 5th Edition.

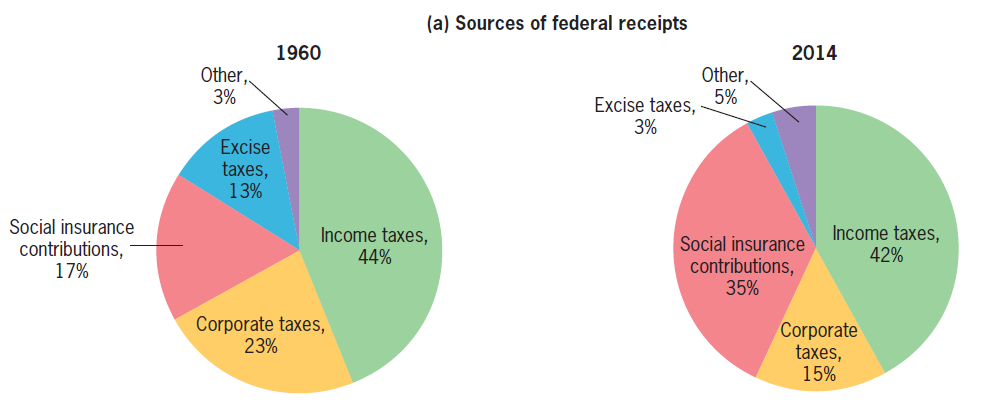

Federal Government Receipts: 1960 vs 2014

From: Jonathan Gruber (2016). Public Finance and Public Policy, 5th Edition.

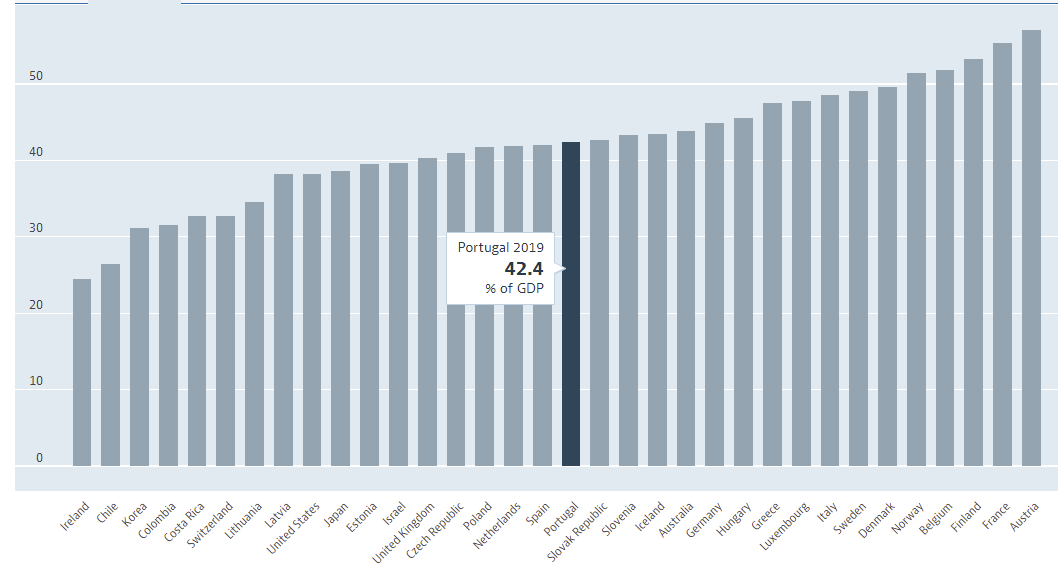

Public Spending as a % of GDP (OECD, 2019)

No, Portugal is not the country with the highest Public Spendind/GDP ratio. OECD

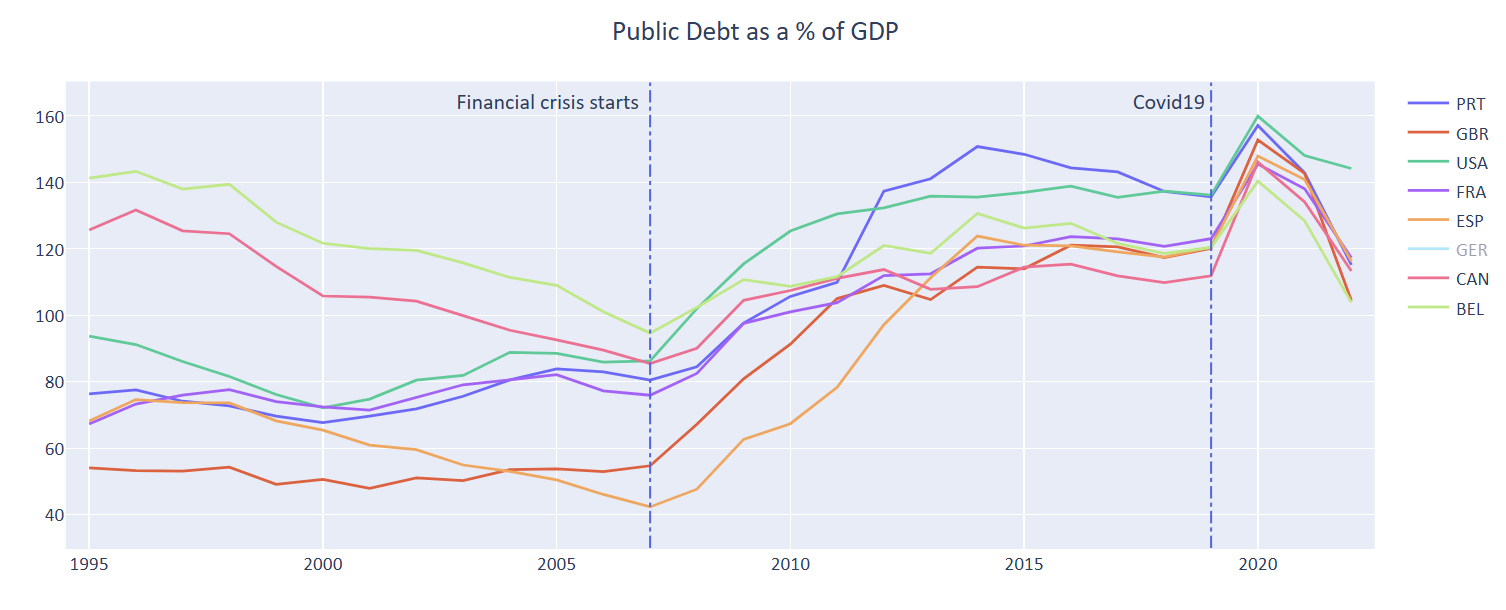

Public Debt as a % of GDP

Public debt/GDP ratio changes drastically with external shocks. From: OECD

USA: Federal Budget vs Federal Debt

A paradox: the US government run a deficit for decades, yet its debt/GDP ratio declined until 1981. From: FRED

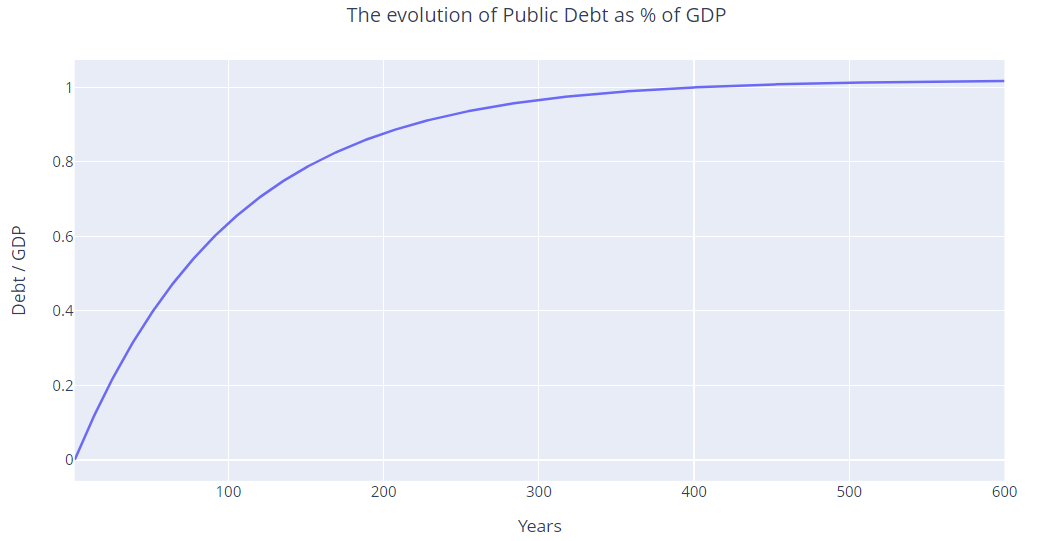

Public Debt Sustainability: An Exercise

Pessimistic scenario: \(p=0.1\%, g=2\%, r_p=1\%\). Surprise … the time span.

The Shadows Behind Public Debt

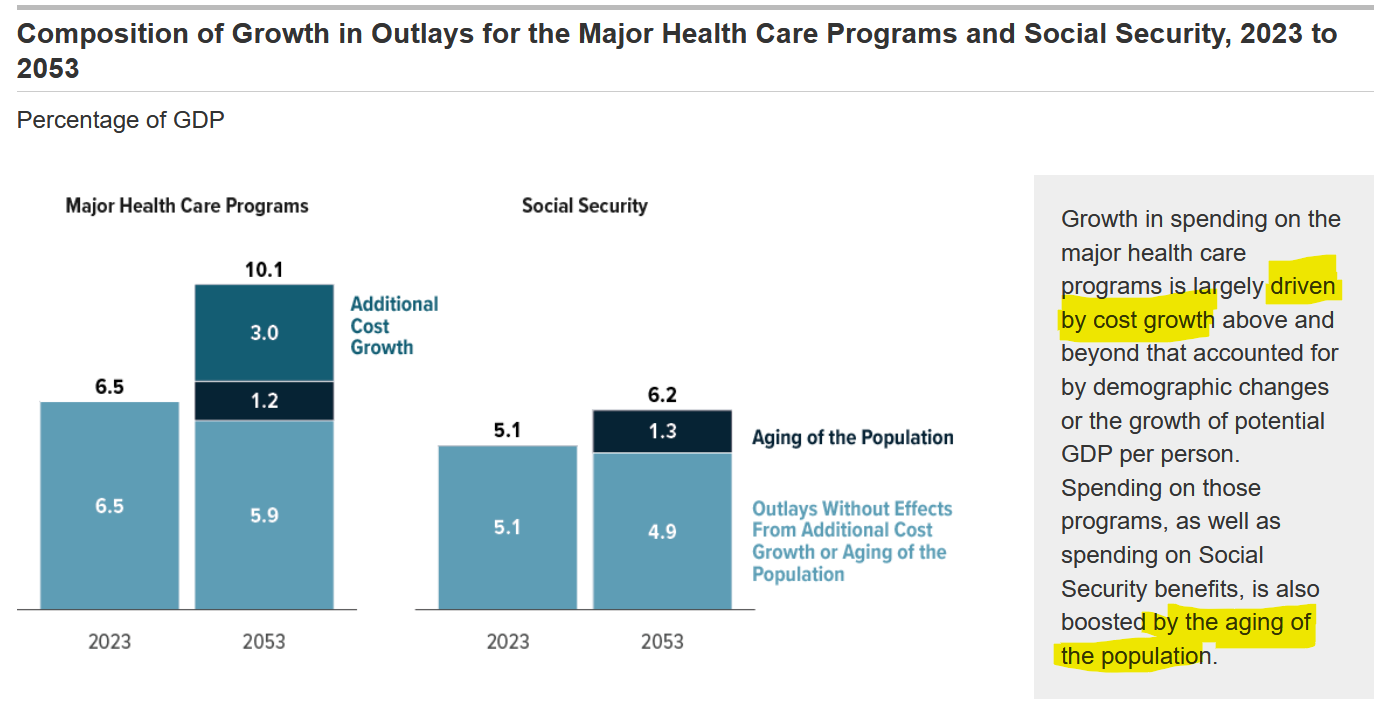

The “Problem”: the Aging of the Population

For the Congressional Budget Office aging is the major problem for public finances in the USA.

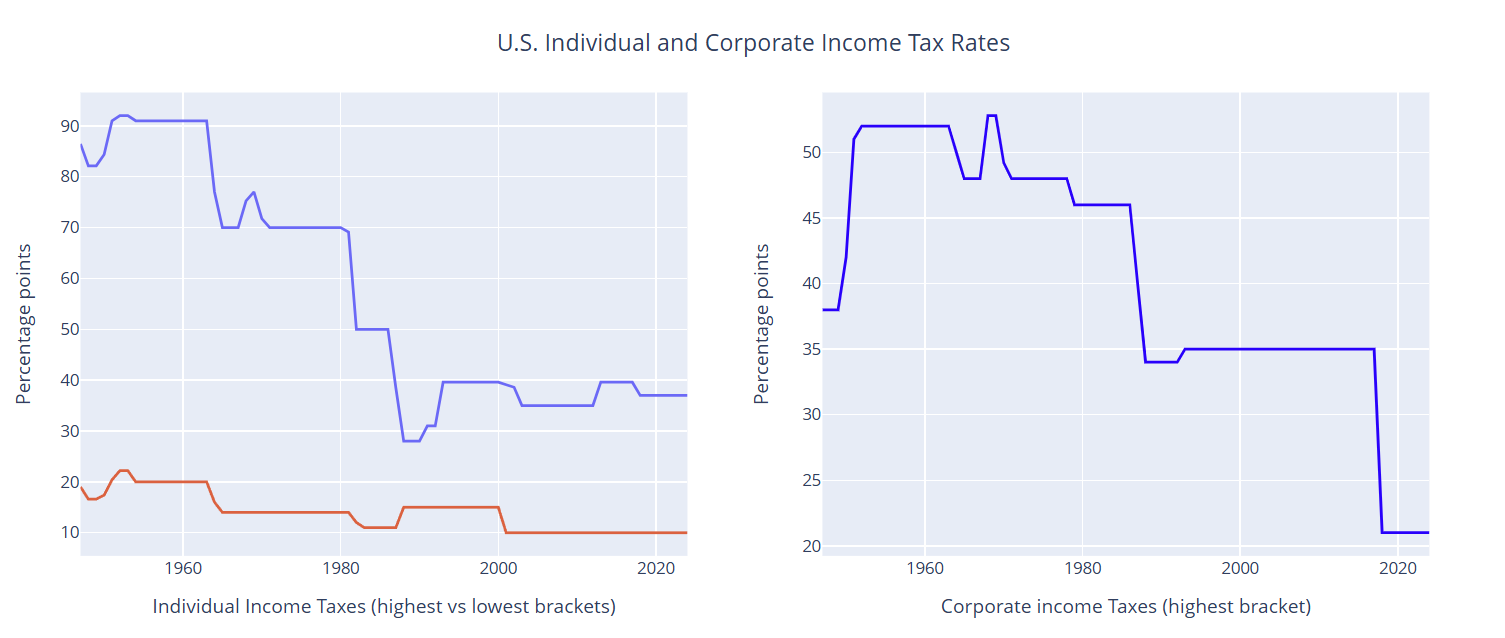

Another “Problem”: Income Taxation

Since the early 1960s, the highest tax brackets for individual and corporate income have dropped dramatically.

Discretionary Spending Has Come Down

Mandatory Spending Has Not Skyrocket

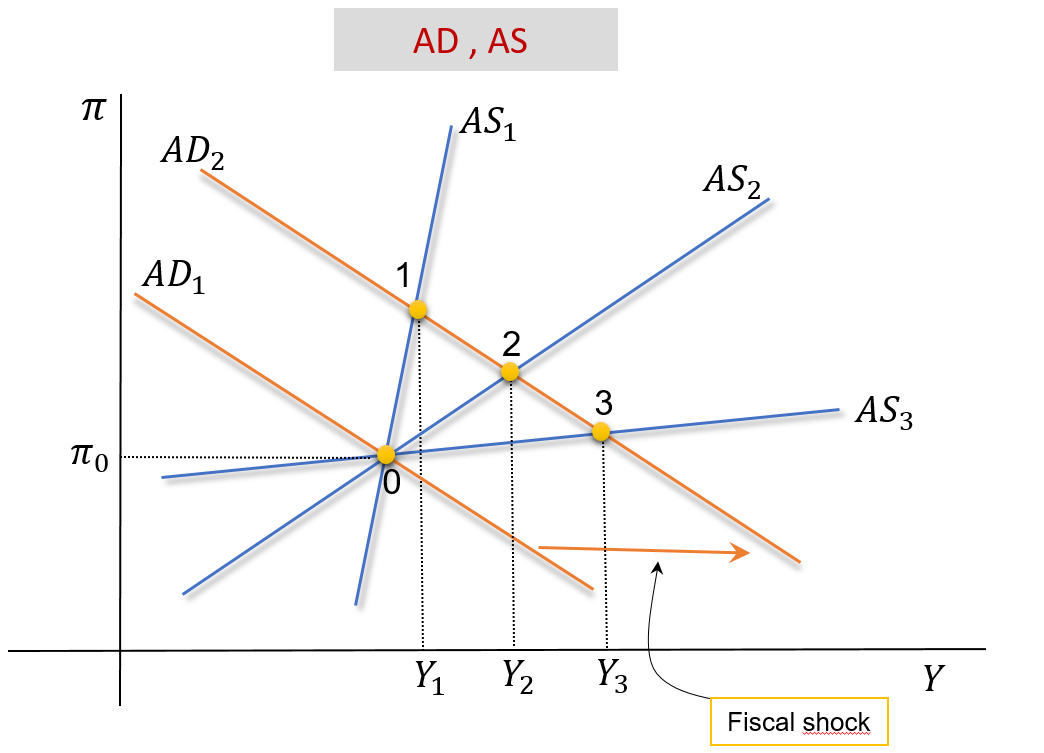

Fiscal Multiplier: The Intuition

The higher is the AS’s slope, the lower will be the fiscal multiplier.

- The same fiscal expansion will have a lower impact on \(Y\) if the AS is steeper.

- \[\Delta Y_1 < \Delta Y_2 < \Delta Y_3\]

- Higer slope of the AS: higher \(\gamma\)