Macroeconomic Policy & Extreme Shocks

Week 10

April 27, 2026

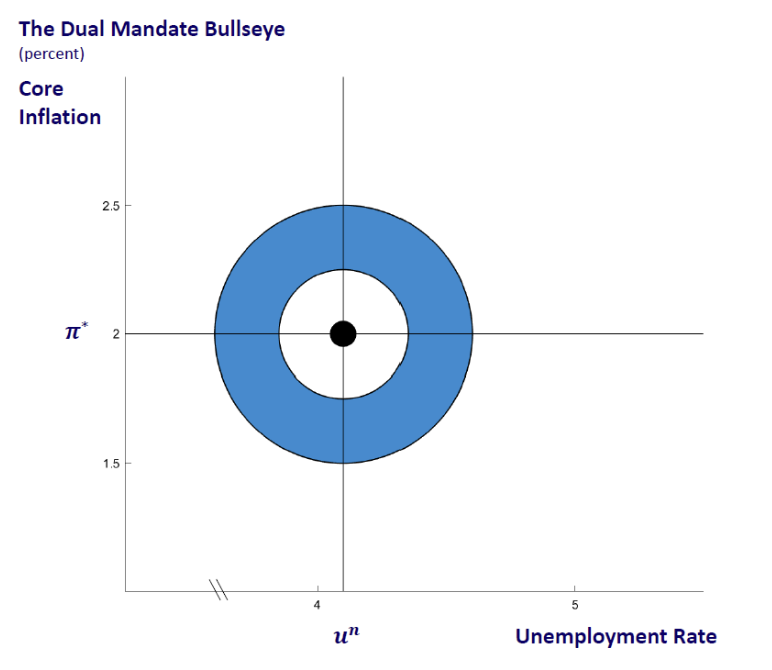

The Fed’s Dual Mandate

The Fed’s dual mandate according to the Federal Reserve Bank of Chicago

The FRB of Chicago calls the target inflation rate by \(\pi^*\)

We call it \(\pi^{_T}\)

The meaning is the same

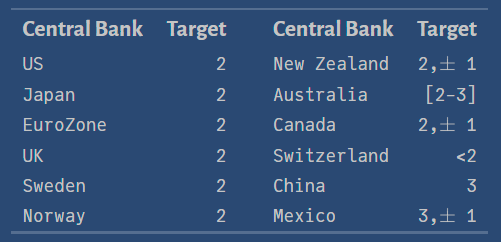

Inflation Rate Target

All central banks in advanced countries have an optimal value for inflation they want to achieve. This is called the inflation target:\[\color{blue}{\pi^{_T}}\]

\(~~~~~~~~~~~~~~~~~~~~~\)

Source: Central Bank News

The Textbook Rule vs the Fed Funds Rate

We set: \(\lambda=0.5, \overline{r}=2\). The textbook rule performs very badly.

The Taylor Rule vs the Fed Funds Rate

Weights: 0.5 for the output-gap, 0.5 for the inflation-gap.

The New Taylor Rule vs the Fed Funds Rate

Weights: 1.0 for the output-gap, 0.5 for the inflation-gap: it performs better

Explosive Inflation

- In Western countries, inflation reached very high levels … very fast

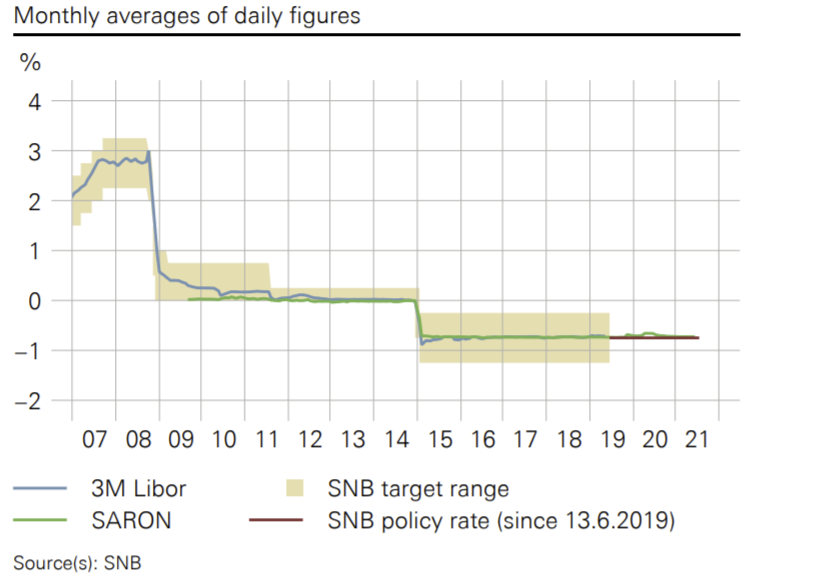

Switzerland: Pinnacle of Financial Stability

- The Swiss National Bank (SNB) kept the interest rate at \(-0.75 \%\) for a long time.

- In September 2022, the SNB decided to raise the rate to \(+0.5 \%\).

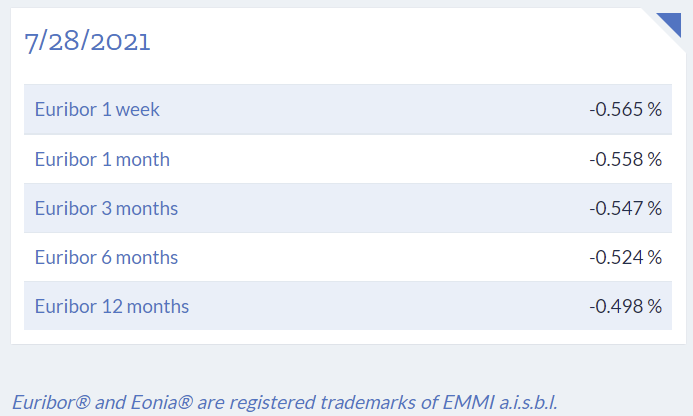

EURIBOR: The Unthinkable

- Euribor rates were negative (for all maturities) in the summer of 2021.

- Currently, they range from \(1.9\%\) and \(2.4\%\)

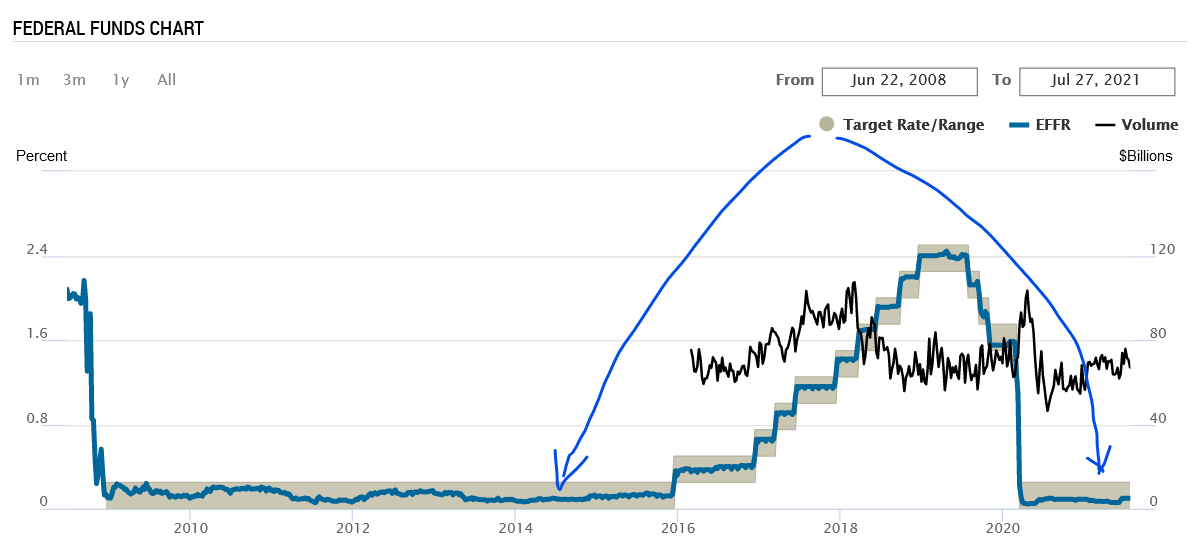

The ZLB: the US case

The Fed Funds Rate is the blue line (it is the overnight market rate); the FED sets the range (the gray interval) in the lower limit (0%). FRB of New York

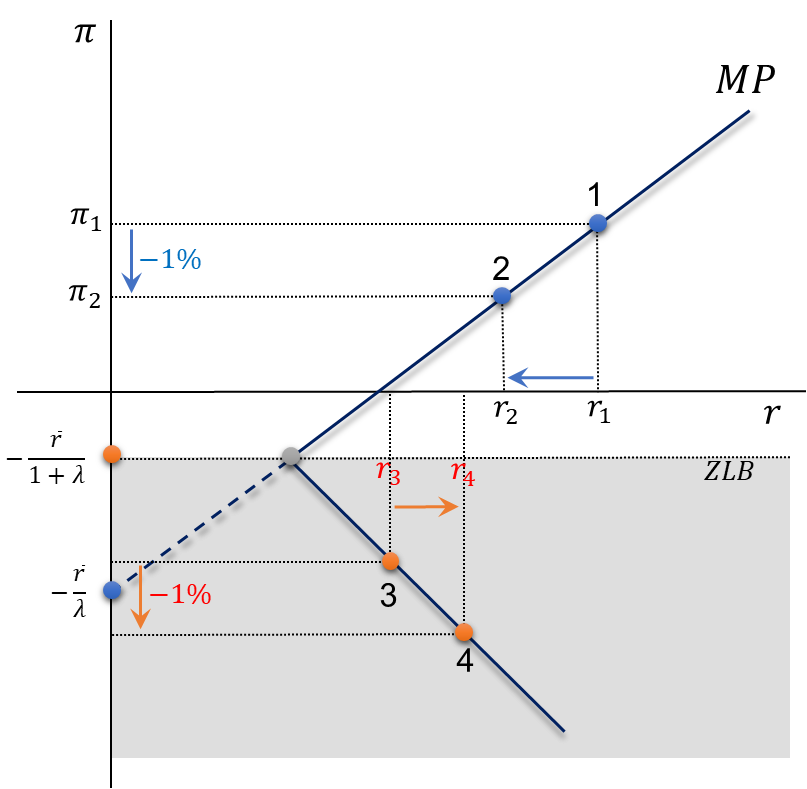

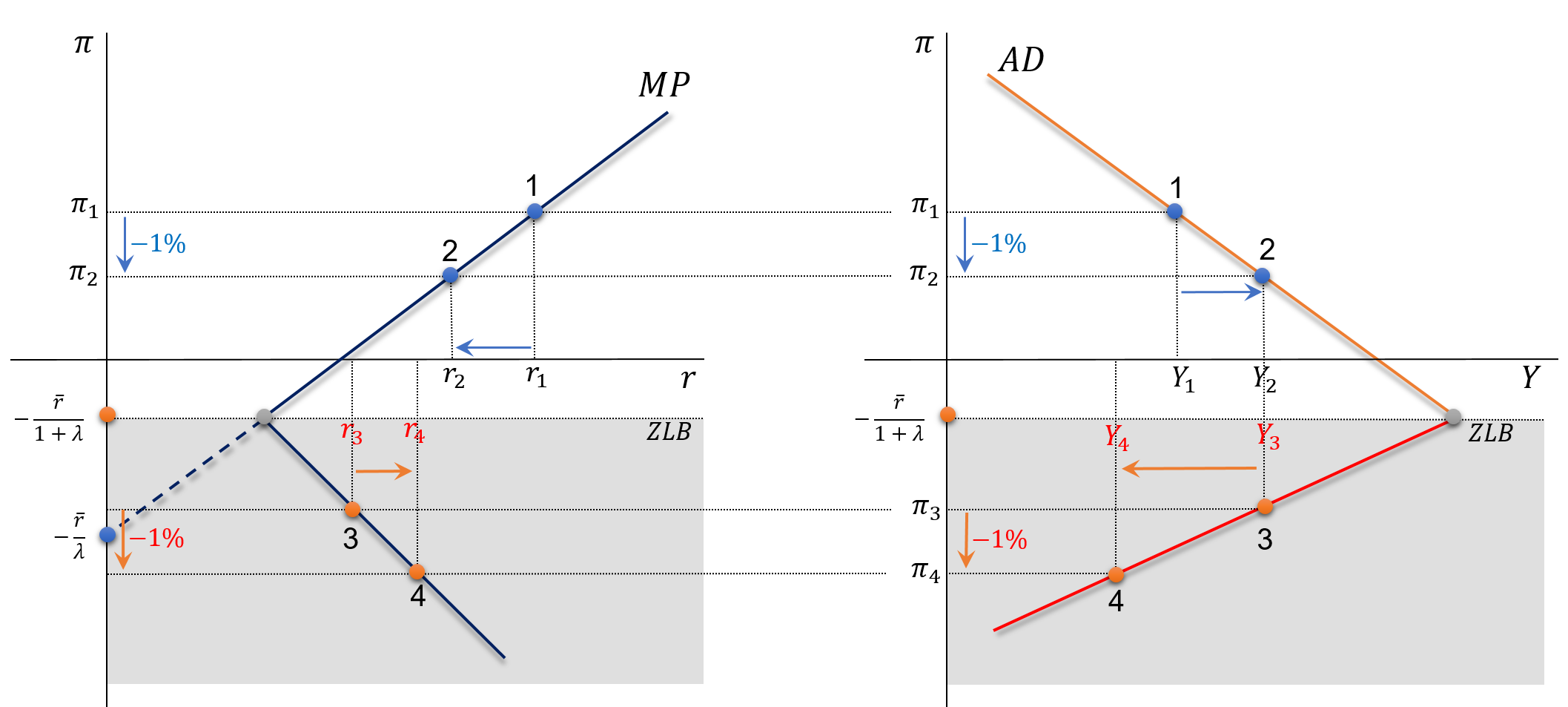

ZLB: Representation of the MP curve

- MP in the normal zone: \[r=\overline{r}- \lambda \pi\]

- MP in the ZLB: \[r=-\pi_{_{ZL}}\]

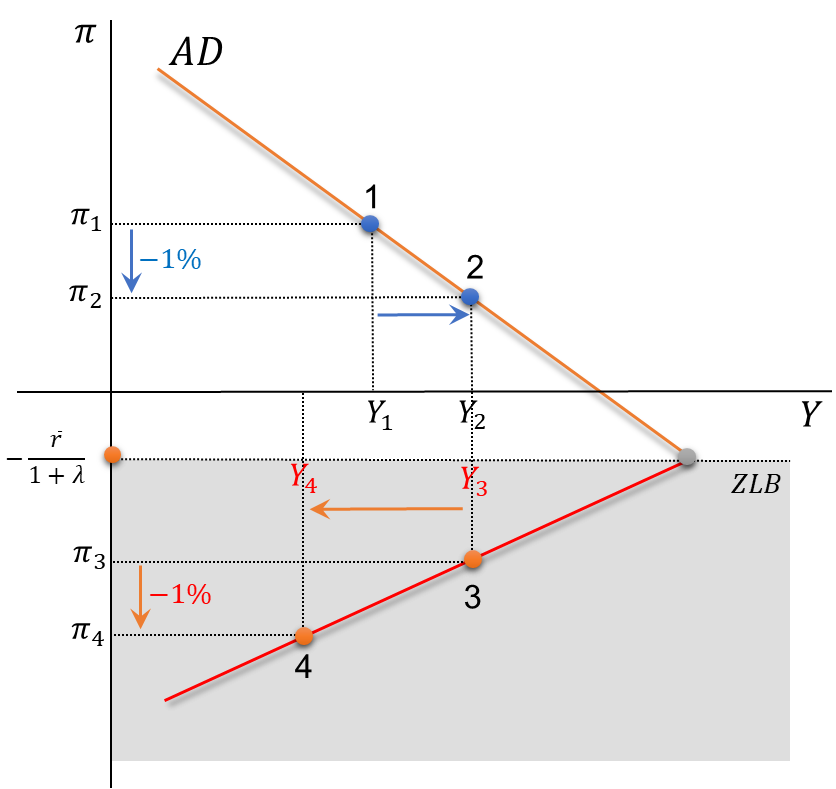

ZLB: Representation of the AD curve

- AD in the normal zone: \[Y=m \cdot \overline{A}-m \cdot \phi \cdot(\overline{r}+\lambda \pi)\]

- AD in the ZLB: \[Y=m \cdot \overline {A}+m \cdot \phi \cdot \pi_{_{Z L}}\]

ZLB: Representation of AD and MP Curves

A reduction in inflation of \(1 \%\) causes different (opposite) impacts upon \(Y\) and \(r\) when comparing the ZLB with the normal zone.

Alice Trough the Looking Glass

Paul Krugman, Nobel Prize winner 2008: the ZLB is a “Alice through the looking glass” experience.

Strange Things I: Deflation Trap

Suppose the economy falls into the ZLB (point \(1_{Z L}\) ). It will end up in the long-term equilibrium \(2_{Z L}\) and remain trapped there forever.

Strange Things II: Secular Stagnation

Suppose a big negative demand shock forces the economy to move to point 2. In the long term, it will end up at point 3.