Macroeconomic Policy\(:\) The AD/AS/MP Model

Week 09

April 28, 2025

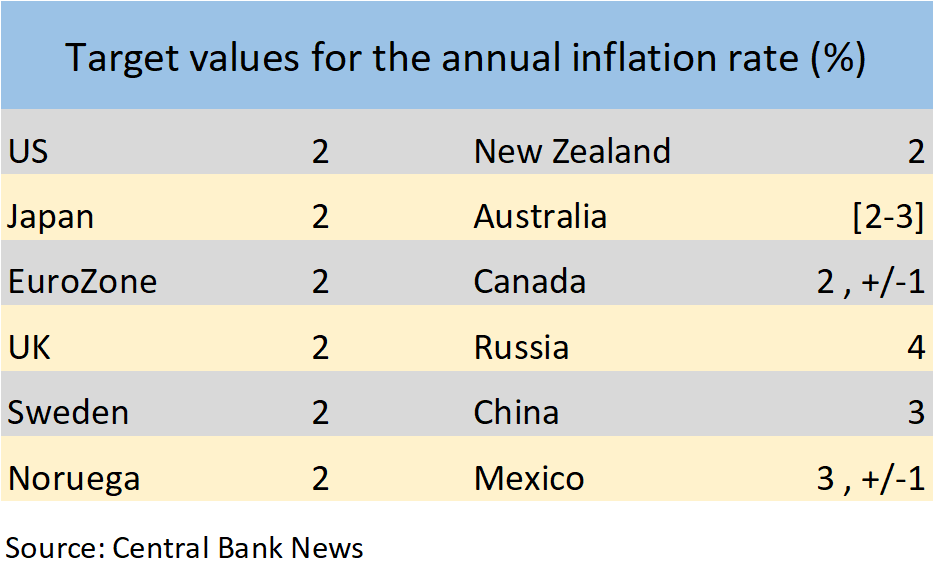

Inflation Rate Target

All central banks in advanced countries have an optimal value for inflation they want to achieve. This is called the inflation target:\[\color{blue}{\pi^{_T}}\]

\(~~~~~~~~~~~~~~~~~~~~~~~~\)

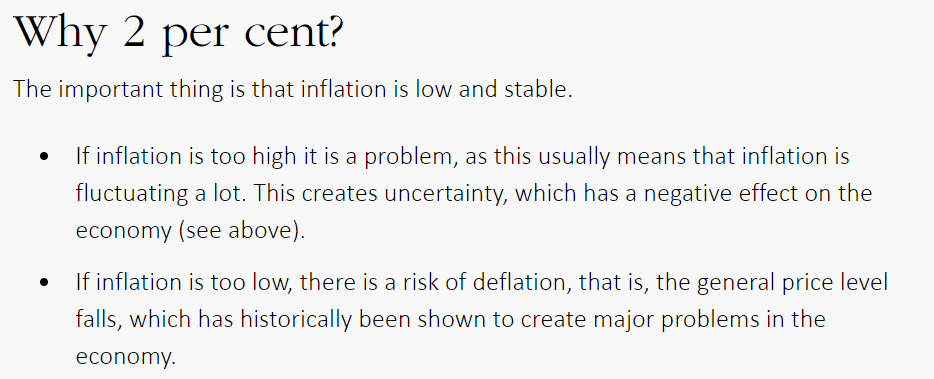

Why \(2\%\) Inflation?

According to the Swedish Central Bank (Sveriges Central Bank):

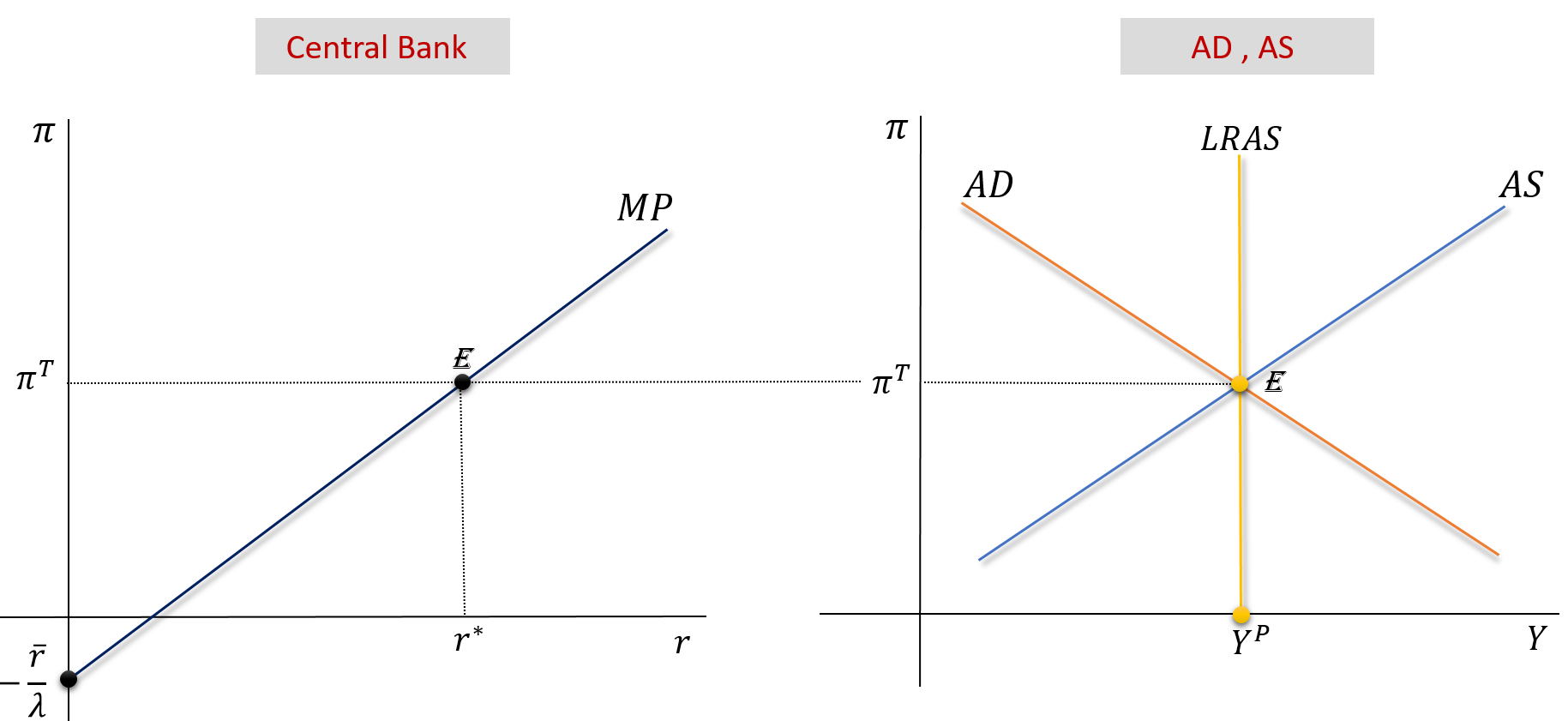

Long-Run = Short-Run Equilibrium

The central bank sets \(i\) such that \(r\) will lead to the “divine coincidence”: \(Y=Y^P \ , \ U=U^n \ \ , \ \pi=\pi^{_T} \ \). See an animated version here

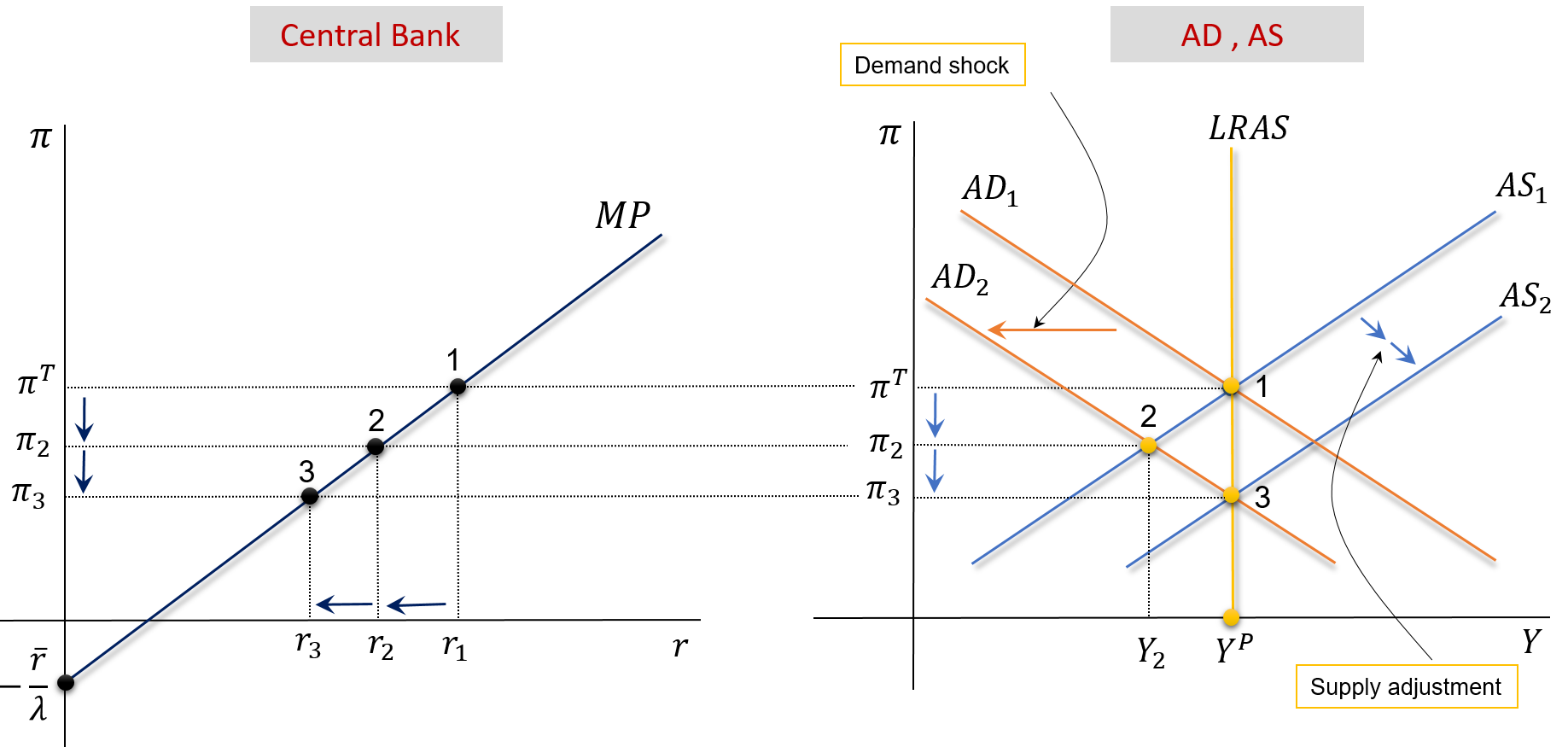

Soft Reaction by the Central Bank

Consider that \(\overline{A} \downarrow\). Then \(\pi \downarrow\), the central bank reduces \(r\) and accepts \(\pi<\pi^{_T}\). See the animated version here

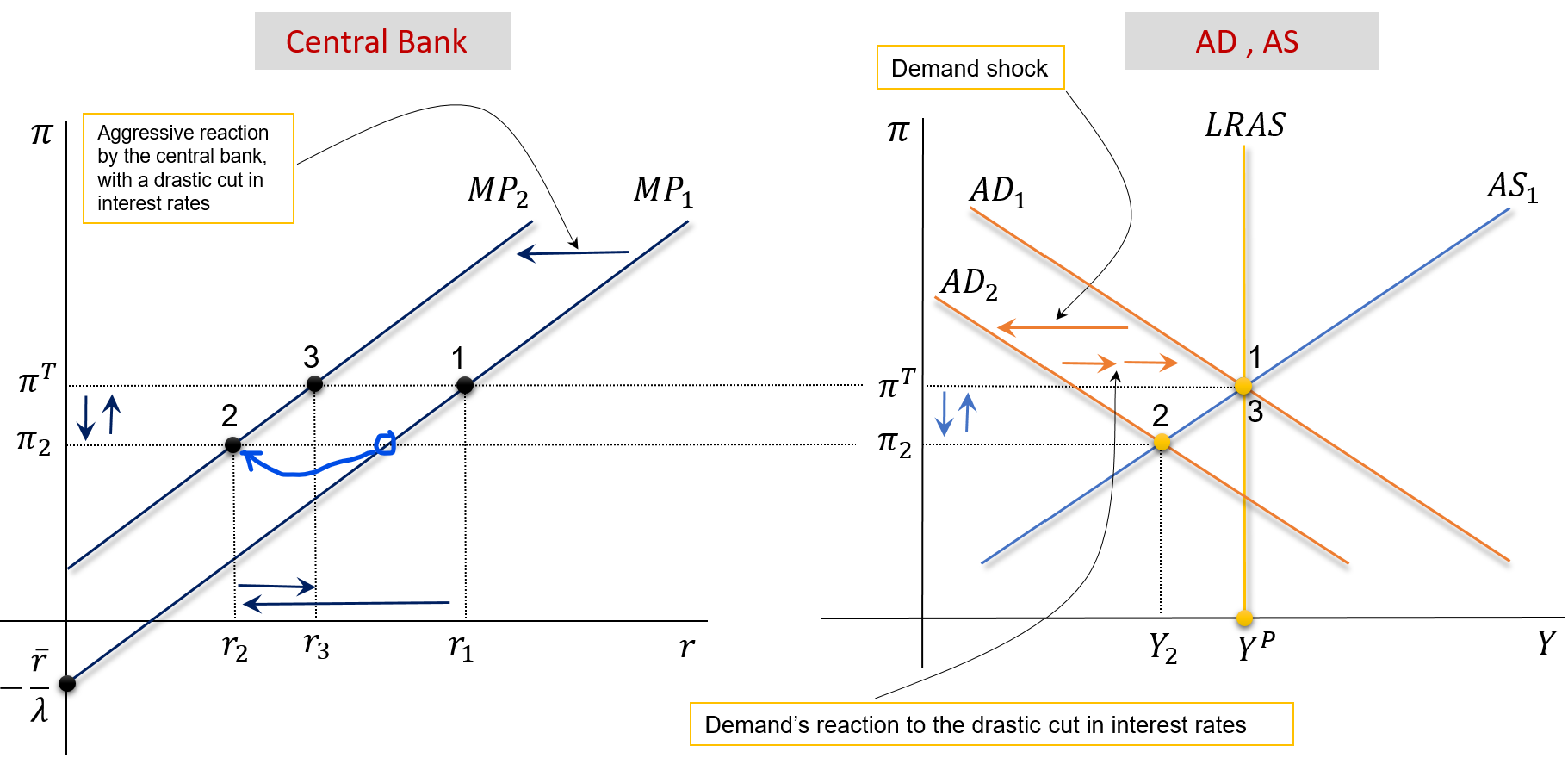

Aggressive Reaction by the Central Bank

Consider that \(\overline{A} \downarrow\).Then \(\pi \downarrow\), the central bank drastically \(r \downarrow\) and forces \(\pi \rightarrow \pi^{_T}\). See the animated version here

Permanent AS Shock: Soft Response

Suppose international oil prices increase and don’t go down. Then \(\pi \uparrow\), the central bank increases \(r\) and accepts \(\pi>\pi^{_T}\). See the animated version here

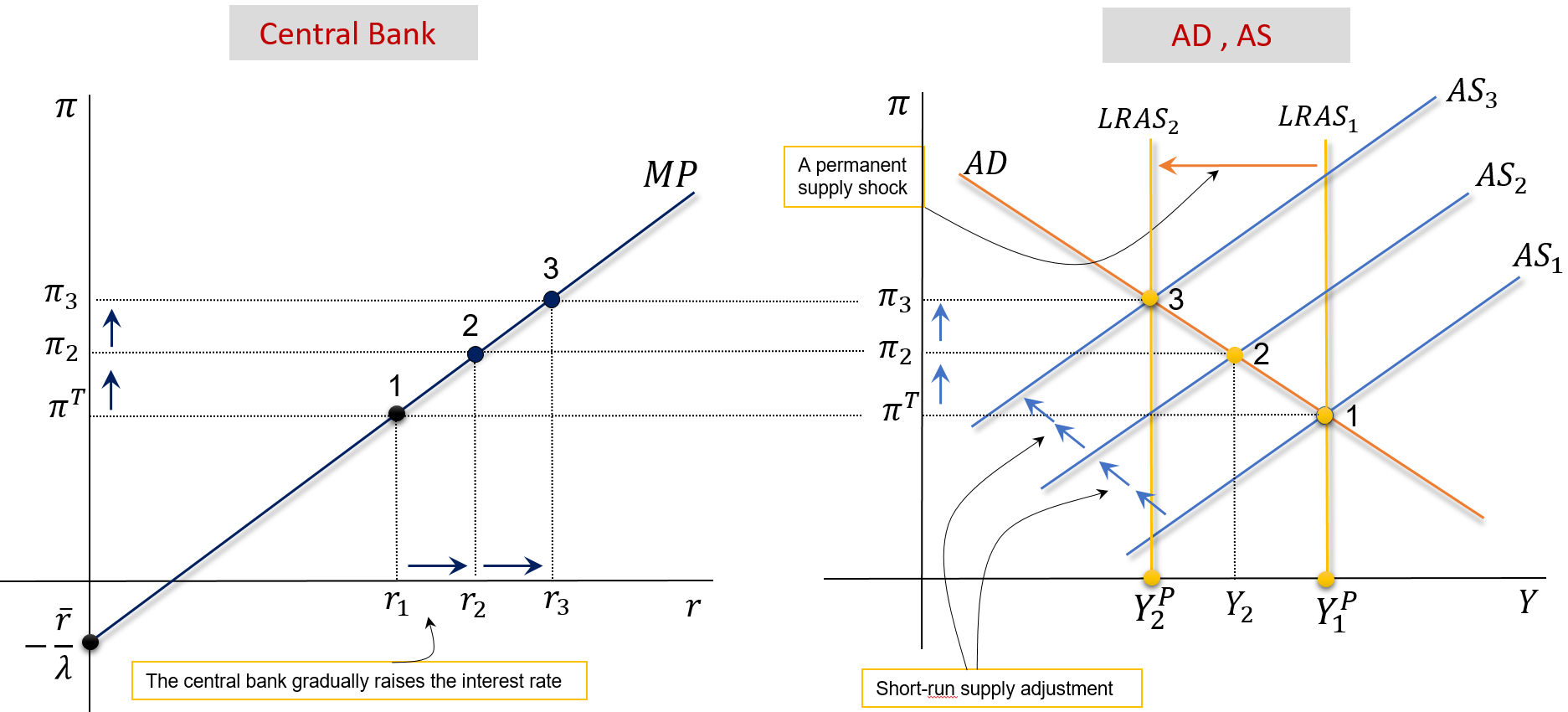

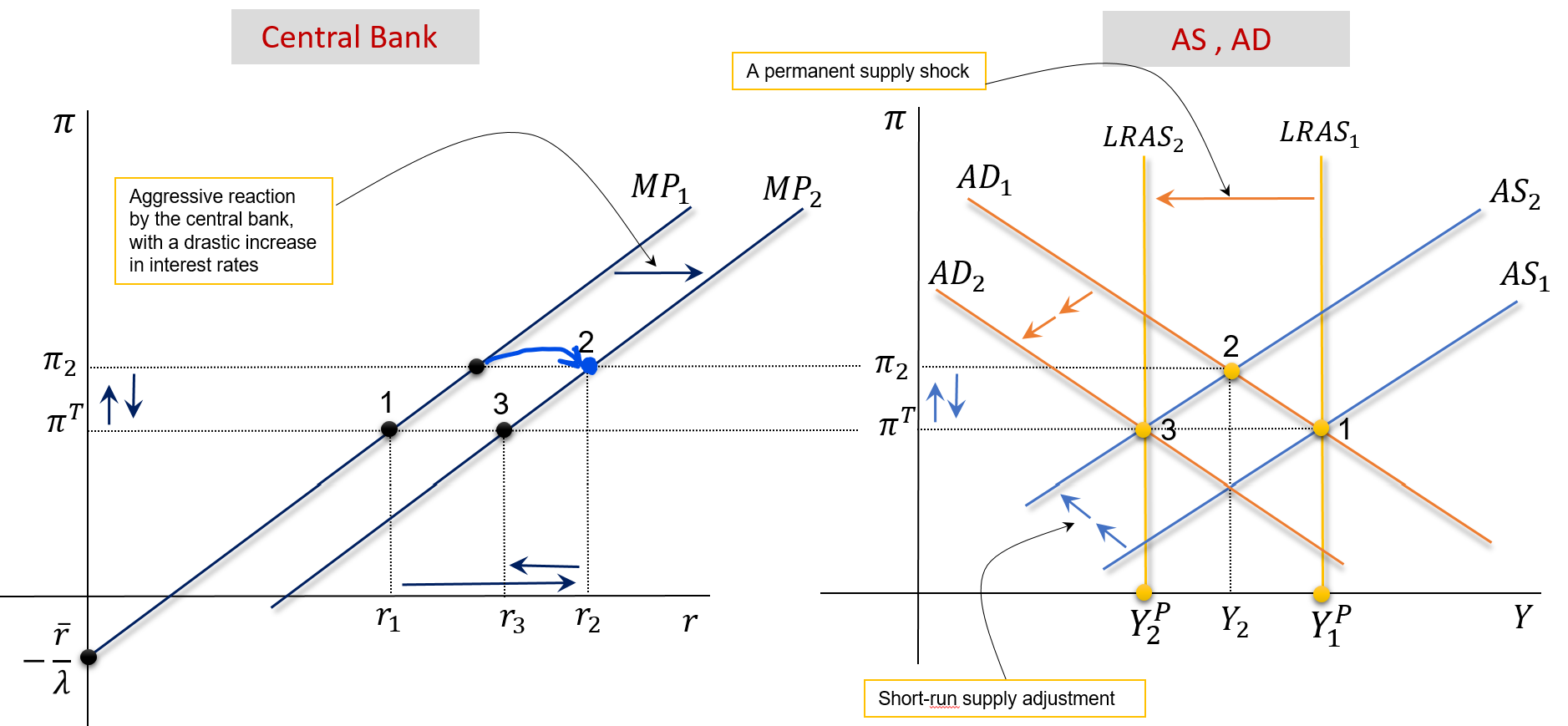

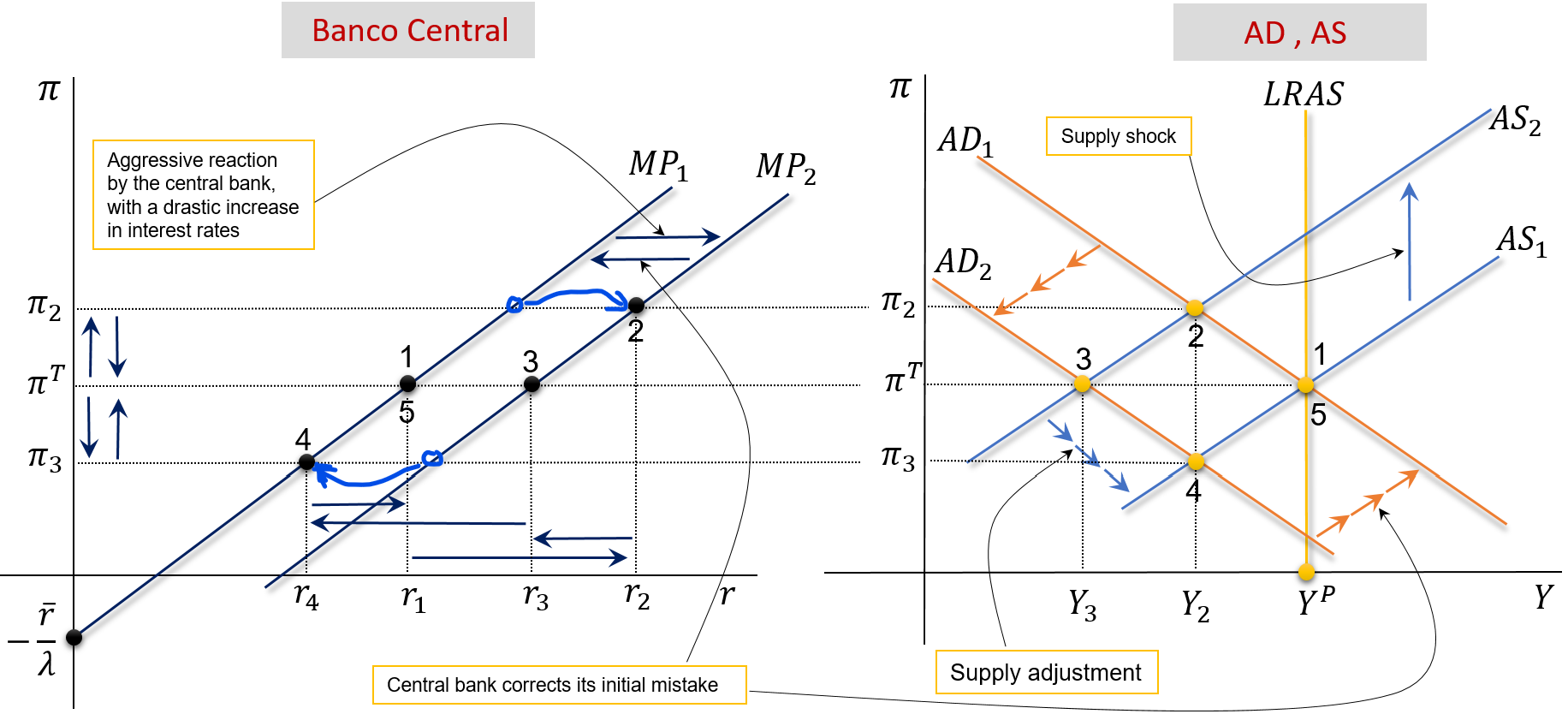

Permanent AS Shock: Aggressive Response

Suppose oil prices increase and don’t go down. Then \(\pi \uparrow\), the central bank drastically increases \(r\) to avoid \(\pi>\pi^{_T}\). See the animated version here

Temporary AS Shock: Soft Response

Suppose that oil prices increase temporarily \((\rho \uparrow)\). The CB softly reacts to the shock. See the animated version here

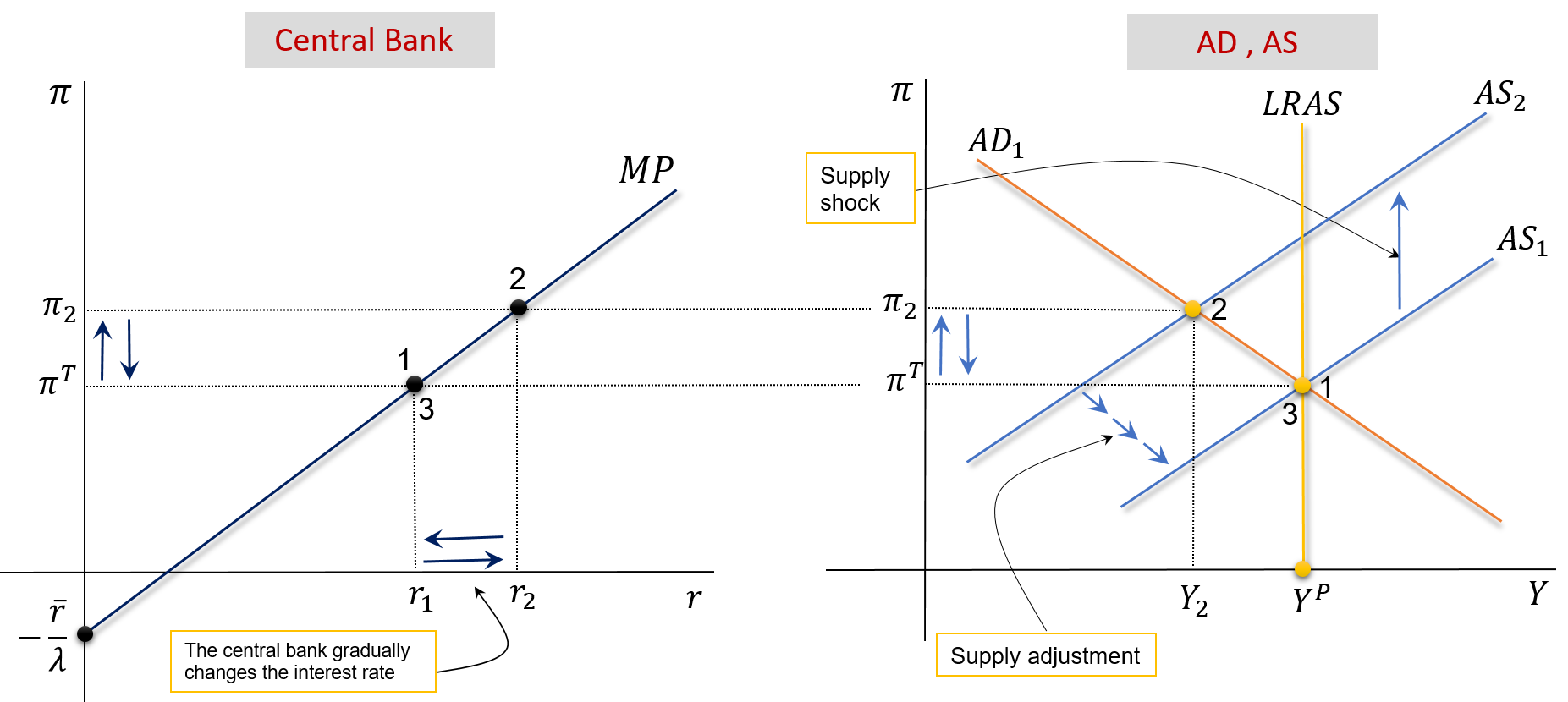

Temporary AS Shock: Aggressive Response

Suppose that oil prices increase temporarily \((\rho \uparrow)\). The CB aggressively reacts with a sharp increase in interest rates. See the animated version here

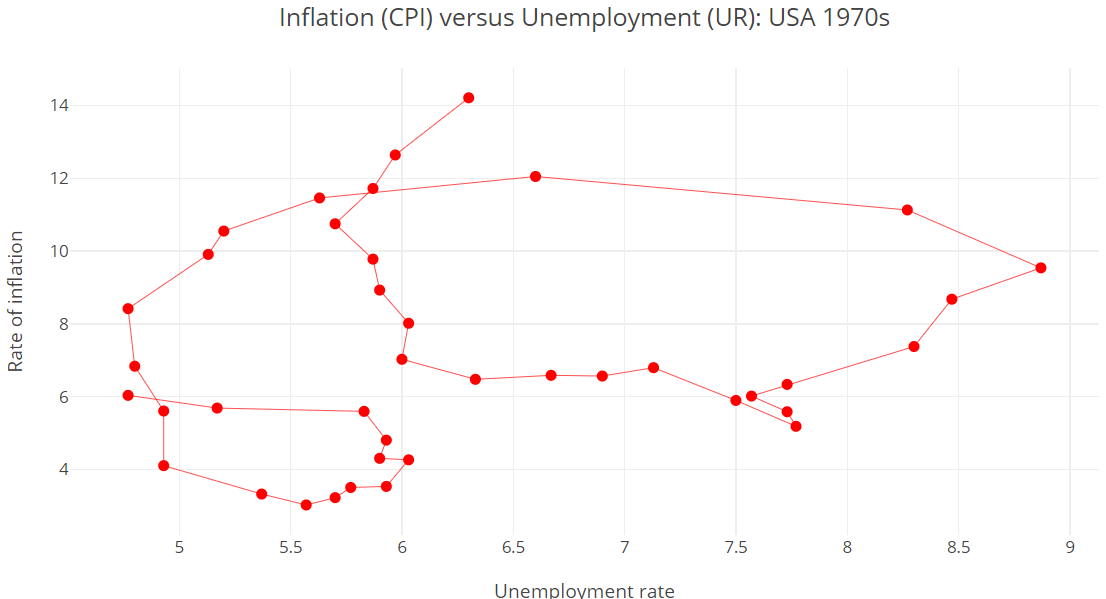

Inflation Loops in the 1970s: USA

The Phillips Curve of the 1970s seems to confirm the circular movement of inflation seen in the previous figure (points: \(1,2,3,4,5\) ).

Readings

Read Chapter 13 of the adopted textbook:

Frederic S. Mishkin (2015). Macroeconomics: Policy & Practice, Second Edition, Pearson Editors.

![]()